The 4 C’s of Internal Audit: A Comprehensive Guide

Introduction

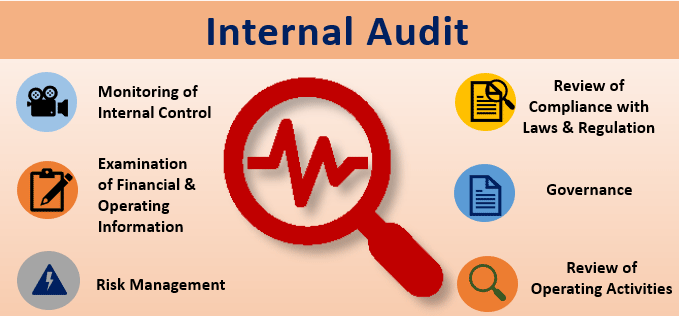

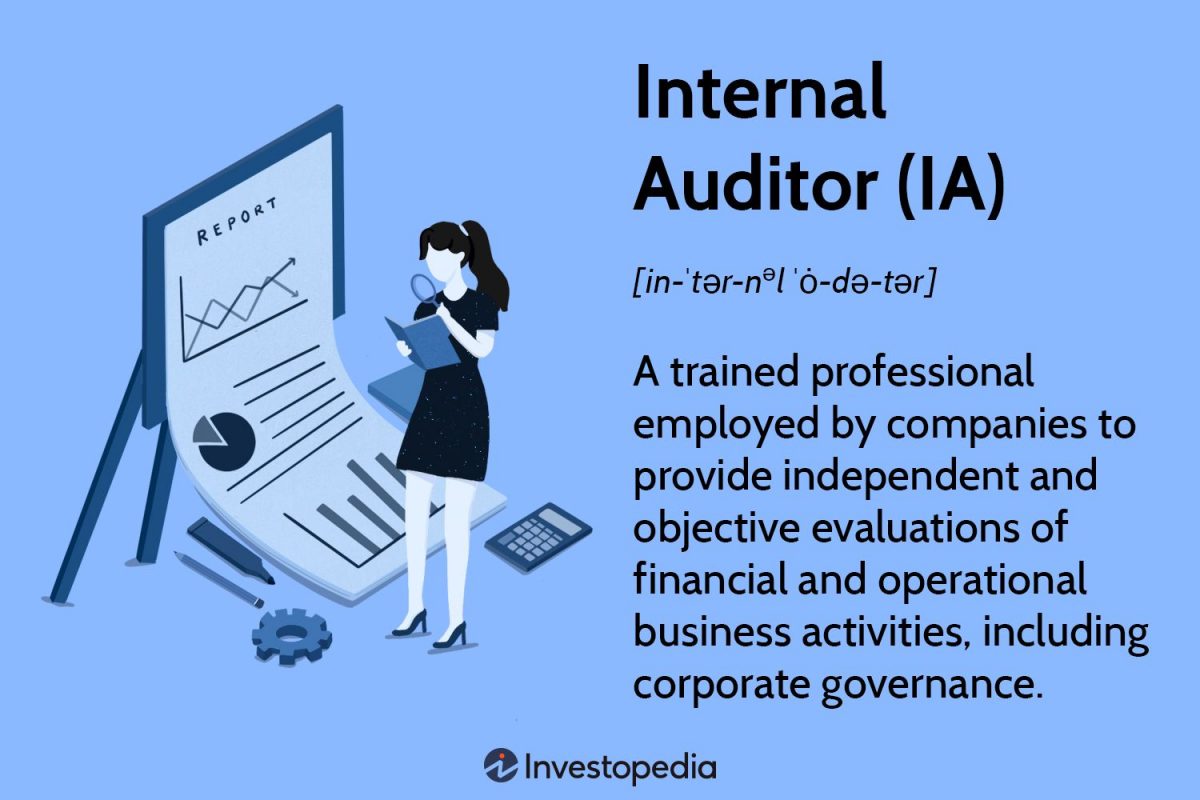

Internal audit is a crucial function within organizations that plays a vital role in evaluating and improving their internal controls, risk management processes, and overall governance. To ensure a systematic and effective approach, internal auditors often refer to the 4 C’s framework. These 4 C’s—Competence, Confidentiality, Compliance, and Communication—serve as guiding principles for internal auditors to carry out their responsibilities with integrity and proficiency. In this article, we will delve into each of these C’s and explore their significance in the realm of internal audit.

Competence: The Foundation of Internal Audit

Competence forms the bedrock of internal audit. It refers to the knowledge, skills, and expertise possessed by internal auditors to perform their duties effectively. Competent auditors are equipped with a deep understanding of accounting principles, auditing standards, industry-specific regulations, and the organization’s operations. They continually enhance their expertise through professional development and stay up-to-date with emerging trends and best practices.

What are the 4 C’s of internal audit?

A competent internal auditor possesses strong analytical and problem-solving abilities, as well as effective communication and interpersonal skills. These qualities enable auditors to identify risks, evaluate controls, and provide valuable insights to management. By maintaining a high level of competence, internal auditors contribute to the overall success of their organizations by ensuring effective risk management and control processes.

Confidentiality: Safeguarding Sensitive Information

Confidentiality is an essential aspect of internal audit, as auditors handle sensitive and confidential information while performing their duties. Internal auditors often have access to privileged data, such as financial records, proprietary information, and strategic plans. Safeguarding this information is vital to maintain the trust and credibility of the internal audit function.

Auditors must adhere to strict ethical standards and legal requirements to ensure the confidentiality of the information they come across during their audits. They should exercise caution when sharing information and only disclose it to authorized individuals within the organization. Failure to maintain confidentiality can lead to reputational damage, legal consequences, and compromised audit outcomes. Therefore, internal auditors must prioritize confidentiality and establish robust procedures to protect sensitive data.

Compliance: Upholding Laws and Regulations

Compliance is a critical component of internal audit. Internal auditors play a crucial role in ensuring that organizations adhere to applicable laws, regulations, and internal policies. They assess the effectiveness of controls and processes in place to mitigate legal and regulatory risks and provide recommendations for improvement.

By evaluating compliance, internal auditors help organizations minimize the risk of penalties, fines, and legal actions. They also contribute to the establishment of a strong ethical culture within the organization. Internal auditors should have a comprehensive understanding of relevant laws and regulations, including industry-specific requirements, to effectively evaluate compliance and provide reliable assurance to management and stakeholders.

Communication: Building Bridges and Sharing Insights

Effective communication is a key attribute of successful internal auditors. Communication encompasses both the ability to convey information clearly and the capacity to actively listen to others. Internal auditors interact with various stakeholders, including management, employees, and external parties. They must effectively communicate audit findings, recommendations, and insights to ensure their message is understood and acted upon.

Clear communication helps build relationships and foster collaboration with management and other stakeholders. Internal auditors should present their findings in a concise and understandable manner, using appropriate language and avoiding technical jargon. They should also actively listen to stakeholders’ concerns, gather relevant information, and incorporate feedback into their audit processes. For a internal audit agent in ashfield read on.

Conclusion

In conclusion, the 4 C’s of internal audit—Competence, Confidentiality, Compliance, and Communication—form the pillars of a robust and effective internal audit function. Competence ensures that internal auditors possess the necessary knowledge and skills to perform their duties with proficiency. Confidentiality emphasizes the importance of safeguarding sensitive information and maintaining the trust of stakeholders. Compliance ensures adherence to laws, regulations, and internal policies, minimizing legal and regulatory risks. Lastly, communication is essential for building relationships, conveying findings, and sharing insights effectively.

By adhering to these 4 C’s, internal auditors contribute to the overall success of their organizations. They help identify and mitigate risks, improve internal controls, and provide valuable insights for decision-making. Internal audit plays a vital role in enhancing governance, transparency, and accountability within organizations, ultimately leading to improved organizational performance and stakeholder confidence.