What is an Example of a Financial Analysis?

Introduction

Financial analysis is a crucial tool used by businesses and investors to evaluate the financial health and performance of a company. It involves examining financial statements, ratios, and other relevant data to gain insights into the company’s profitability, liquidity, solvency, and overall financial stability. This article will provide an example of a financial analysis and explain how it can be conducted to assess a company’s financial condition.

Understanding Financial Analysis

Financial analysis involves a comprehensive review of a company’s financial statements, which typically include the balance sheet, income statement, and cash flow statement. These statements provide valuable information about a company’s assets, liabilities, revenues, expenses, and cash flow. By analyzing these statements, investors and analysts can assess the company’s financial performance over a specific period and make informed decisions.

Example: XYZ Company

To illustrate the process of financial analysis, let’s consider an example of XYZ Company, a fictional manufacturing company. We will analyze its financial statements for the fiscal year 20XX to evaluate its financial position and performance.

1. Assessing Profitability

Profitability analysis focuses on understanding a company’s ability to generate profits and maintain sustainable earnings growth. Key metrics used in profitability analysis include gross profit margin, operating profit margin, and net profit margin.

Gross Profit Margin

The gross profit margin indicates the percentage of revenue that remains after deducting the cost of goods sold (COGS). It is calculated by dividing gross profit by revenue and multiplying the result by 100.

For example, if XYZ Company’s gross profit is $500,000 and its revenue is $1,000,000, the gross profit margin would be 50% ($500,000 / $1,000,000 x 100). A higher gross profit margin indicates better cost control and pricing power.

Operating Profit Margin

The operating profit margin measures a company’s profitability after accounting for all operating expenses. It is calculated by dividing operating profit by revenue and multiplying the result by 100.

What is an example of a financial analysis?

Suppose XYZ Company’s operating profit is $200,000 and its revenue is $1,000,000. In that case, the operating profit margin would be 20% ($200,000 / $1,000,000 x 100). This metric helps evaluate the company’s operational efficiency.

Net Profit Margin

The net profit margin reflects the company’s profitability after considering all expenses, including taxes and interest. It is calculated by dividing net profit by revenue and multiplying the result by 100.

If XYZ Company’s net profit is $100,000 and its revenue is $1,000,000, the net profit margin would be 10% ($100,000 / $1,000,000 x 100). A higher net profit margin indicates better overall financial performance.

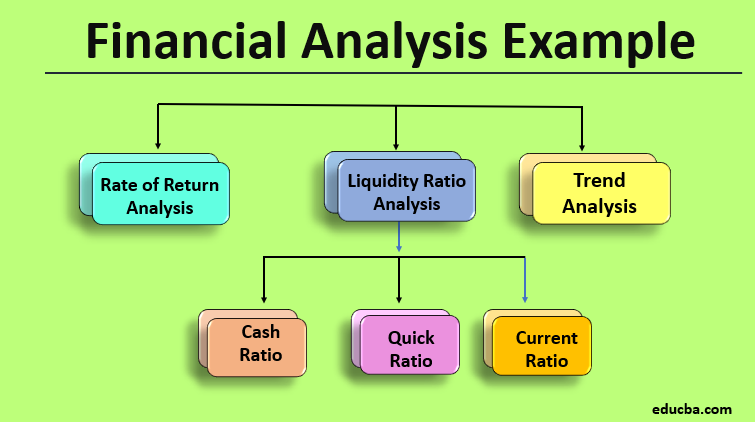

2. Evaluating Liquidity

Liquidity analysis assesses a company’s ability to meet its short-term obligations and manage cash flow effectively. Two commonly used ratios for liquidity analysis are the current ratio and the quick ratio.

Current Ratio

The current ratio measures the company’s ability to pay off its current liabilities using its current assets. It is calculated by dividing current assets by current liabilities.

For example, if XYZ Company has current assets of $500,000 and current liabilities of $300,000, the current ratio would be 1.67 ($500,000 / $300,000). A current ratio above 1 indicates that the company can cover its short-term obligations. https://cbdtax.com.au/

Quick Ratio

The quick ratio, also known as the acid-test ratio, provides a more stringent measure of liquidity. It excludes inventory from current assets since inventory may not be easily convertible to cash. The quick ratio is calculated by dividing current assets minus inventory by current liabilities.

Suppose XYZ Company has current assets of $500,000, inventory of $200,000, and current liabilities of $300,000. The quick ratio would be 1.00 (($500,000 – $200,000) / $300,000). A higher quick ratio suggests a stronger ability to meet short-term obligations without relying heavily on inventory.

3. Analyzing Solvency

Solvency analysis examines a company’s long-term financial stability and its ability to meet long-term debt obligations. The debt-to-equity ratio and interest coverage ratio are commonly used in solvency analysis.

Debt-to-Equity Ratio

The debt-to-equity ratio compares a company’s total debt to its shareholders’ equity. It is calculated by dividing total debt by shareholders’ equity.

For example, if XYZ Company has total debt of $1,000,000 and shareholders’ equity of $500,000, the debt-to-equity ratio would be 2.00 ($1,000,000 / $500,000). A higher ratio indicates higher financial leverage and potential higher risk.

Interest Coverage Ratio

The interest coverage ratio measures a company’s ability to cover its interest expenses with its earnings. It is calculated by dividing earnings before interest and taxes (EBIT) by interest expense.

Suppose XYZ Company’s EBIT is $400,000, and its interest expense is $50,000. The interest coverage ratio would be 8.00 ($400,000 / $50,000). A higher interest coverage ratio indicates better solvency and a lower risk of defaulting on debt payments.

Conclusion

Financial analysis is a valuable tool for understanding a company’s financial health and making informed decisions. By examining profitability, liquidity, and solvency, investors and analysts can gain insights into a company’s performance, identify areas for improvement, and assess its financial stability. Conducting a thorough financial analysis allows stakeholders to make sound investment decisions and helps businesses identify strategies to enhance their financial position.