The Golden Rule of Accounting: Understanding the Fundamental Principles

Introduction

What is the golden rule of accountant? Accounting is an essential part of any company since it enables businesses to monitor their financial activities and evaluate their current state of financial health. Accounting is the process of documenting, categorising, and summarising financial data, which helps firms to make educated decisions, conform to applicable tax rules, and convey financial information to various stakeholders.

Nevertheless, accounting is more than just adding up numbers; it also requires adhering to a set of fundamental principles that are collectively referred to as the Golden Rules of Accounting. In the following paragraphs, we will discuss the Golden Rule of Accounting, as well as the reasons why it is essential for businesses to adhere to this rule.

The Golden Rule of Accounting

The Golden Rule of Accounting is a collection of standards that accountants follow when recording financial transactions. These principles are considered to be the industry standard. The rule is based on the principles of double-entry accounting, which demand that every financial transaction be documented in at least two accounts: a debit account and a credit account. This rule requires that every transaction be recorded in at least two accounts. In order to keep the accounting equation in balance, both of the accounts must include amounts that are both identical and opposite to one another.

According to the so-called “Golden Rule” of accounting, “for every debit, there must be a corresponding credit.” This indicates that each transaction needs to be documented in such a way that the total debits and total credits balance out to provide a nett positive amount. This concept is also known as the principle of “balance” or “duality,” and it states that each transaction has two effects on the accounting equation that are equal but opposing to one another.

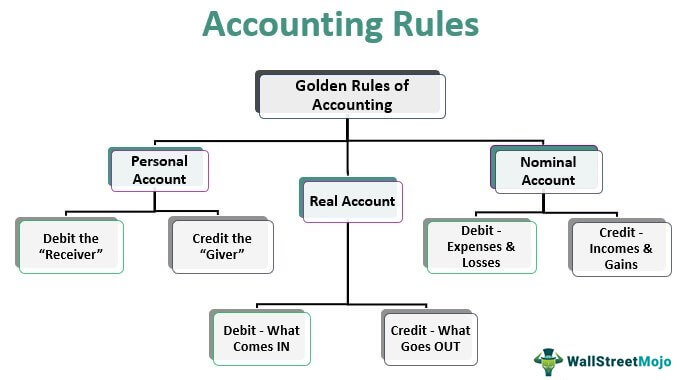

The Three Golden Rules of Accounting

Accountants adhere to these three fundamental criteria in order to guarantee that all monetary transactions are documented accurately and in accordance with the Golden Rule of Accounting.

The requirement that every transaction must have at least one debit and one credit entry is known as the rule of debit and credit. Credits reflect a drop in assets or an increase in liabilities or equity, whereas debits represent an increase in assets or a decrease in liabilities or equity. Debits are used to represent a gain in assets or a decrease in liabilities or equity.

Every transaction must be documented in at least two accounts, with one account being debited and another account being credited, according to the rule of accounts.

The rule of balance states that the total amount of debits should always be equal to the total amount of credits, both for each individual transaction and for the entire accounting period.

Why is the Golden Rule of Accounting important?

Because it ensures that financial transactions are recorded accurately and consistently, the Golden Rule of Accounting is important because it enables businesses to make informed decisions, comply with tax laws, and communicate financial information to stakeholders.

Businesses are able to maintain accurate and up-to-date financial records if they adhere to the Golden Rule of Accounting. These records can assist the company in identifying possible concerns, such as problems with cash flow, and in taking steps to rectify the situation. In addition, maintaining accurate financial records can assist companies in preparing for audits and ensuring compliance with applicable tax regulations.

Furthermore, the Golden Rule of Accounting ensures that financial information is communicated in a consistent manner to stakeholders, such as investors, lenders, and regulators, by requiring that financial statements be prepared in accordance with generally accepted accounting principles. This can assist develop trust and confidence in a company’s financial health and performance, which eventually can lead to expanded chances for investment and expansion. For CBD tax accounting firm near me see here.

Conclusion

To summarise, the “Golden Rule of Accounting” is a key guideline that directs the way financial transactions are recorded by accountants. The rule is based on the principles of double-entry accounting, which demand that every financial transaction be documented in at least two accounts, a debit account and a credit account, with equal and opposite amounts. This rule requires that every transaction be recorded in at least two accounts in order to comply with the requirements of double-entry accounting.

Businesses are able to maintain accurate and up-to-date financial records, comply with applicable tax rules, and convey pertinent financial information to various stakeholders if they follow the “Golden Rule” of accounting. This can assist develop trust and confidence in a company’s financial health and performance, which eventually can lead to expanded chances for investment and expansion.